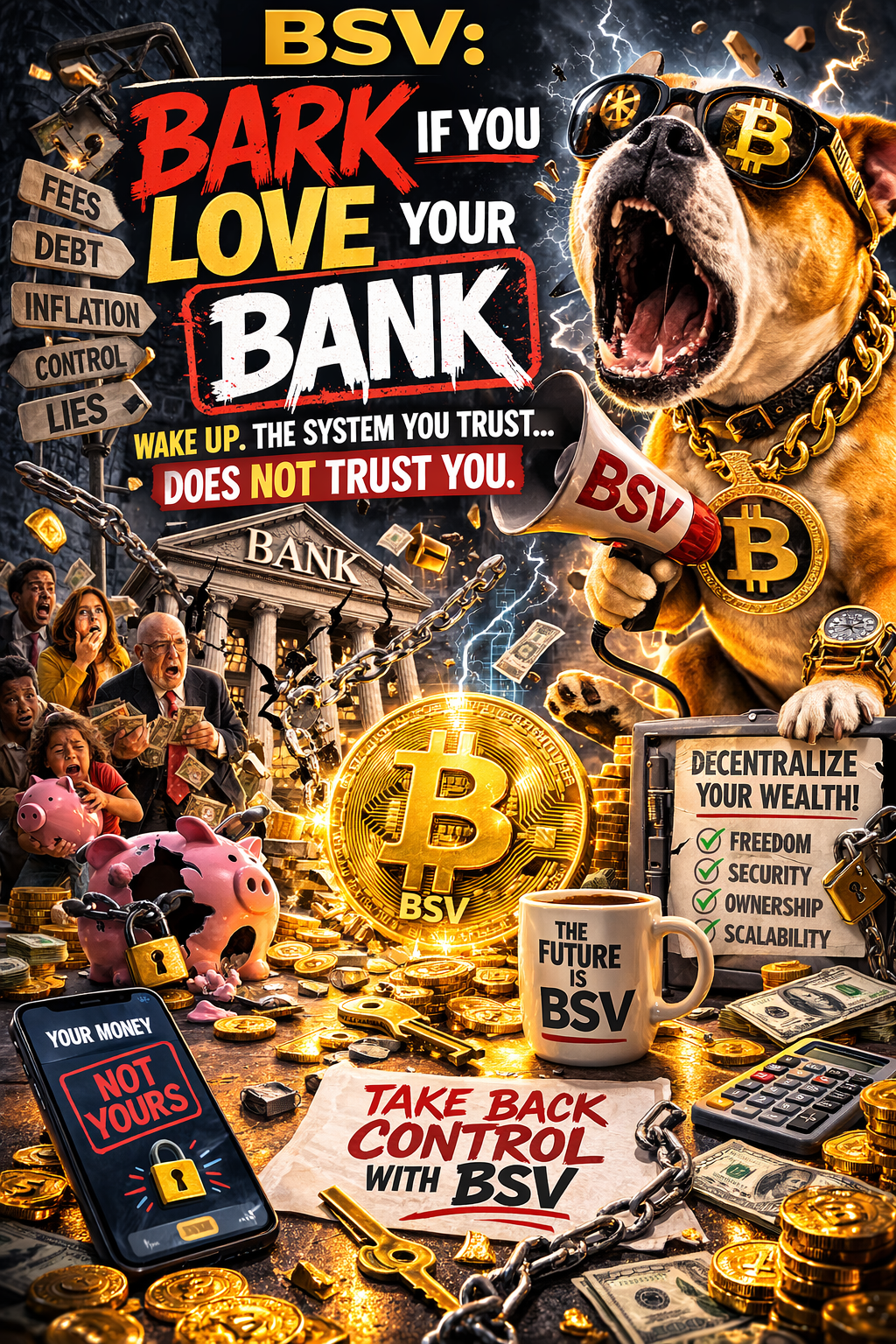

BSV: BARK IF YOU LOVE YOUR BANK 🚨 Bark if you love your ban…

BSV: BARK IF YOU LOVE YOUR BANK

🚨 Bark if you love your bank.

It sounds like a joke.

A slogan you might see on a bumper sticker.

But behind the humor hides a deeper question:

Why do we trust banks so completely?

And more importantly—

Should we?

The Habit of Trust

For centuries, banks have been positioned as guardians of money.

They hold deposits.

They process payments.

They provide loans.

They act as the nervous system of the global economy.

Most people rarely question this structure.

It feels natural.

You deposit money.

You withdraw money.

You trust the system works.

But modern finance reveals a surprising truth:

The money you deposit in a bank is no longer technically yours.

It becomes a liability on the bank’s balance sheet.

You own a claim, not the asset itself.

The Fragile Foundation

Banks operate on a system known as fractional reserves.

This means they hold only a small percentage of deposits as actual liquid reserves.

The rest is loaned out or invested.

Under normal conditions this system functions smoothly.

But during crises, the structure becomes fragile.

If too many depositors attempt to withdraw funds simultaneously, the system strains.

History has witnessed numerous examples:

Banking panics in the 19th century

The Great Depression

The 2008 financial crisis

More recent regional bank failures

These events remind us that financial systems depend heavily on confidence.

When confidence breaks, even large institutions can falter.

The Modern Banking Paradox

Today’s banks are larger and more technologically advanced than ever before.

But they are also more interconnected.

This interconnectedness creates efficiency—but also systemic risk.

Financial institutions rely on:

complex derivative markets

global liquidity networks

central bank backstops

government guarantees

The result is a system where stability often depends on coordinated policy intervention.

In other words, the system works best when nothing goes wrong.

Technology Changes the Equation

The emergence of digital financial technologies has begun to challenge traditional assumptions about banking.

Blockchain networks introduced the idea that value can move across the internet without a centralized intermediary.

Instead of trusting an institution, users rely on cryptographic rules and distributed consensus.

This shift represents a profound conceptual change:

Trust moves from organizations to protocols.

The Bitcoin Idea

Bitcoin was created as a peer-to-peer electronic cash system.

Its core design principles include:

transparency through a public ledger

fixed supply rules

decentralized transaction validation

These characteristics allow value to move globally without requiring traditional banking infrastructure.

However, the ability of such systems to support large-scale economic activity depends heavily on their technical architecture.

The Question of Scale

For digital monetary networks to function as global infrastructure, they must handle significant transaction volumes.

This includes:

everyday payments

microtransactions

enterprise-level settlement

data-driven applications

Bitcoin SV focuses on addressing this challenge by emphasizing high throughput and low transaction costs, aiming to support large-scale economic usage.

In theory, such capabilities could complement or reshape aspects of existing financial infrastructure.

Rethinking the Relationship with Banks

None of this necessarily means banks will disappear.

Banks provide important services:

credit creation

financial intermediation

regulatory compliance

risk management

But technology may gradually change how these services are delivered.

The future financial landscape could involve a mixture of:

traditional institutions

decentralized networks

hybrid models combining both

The Meaning Behind the Joke

“Bark if you love your bank.”

The phrase is humorous, but it highlights a serious point.

Trust in financial institutions has historically been based on tradition and necessity.

Today, new technologies are giving individuals and organizations alternative ways to store and transfer value.

This does not eliminate the need for banks—but it does introduce choice.

And choice can reshape markets.

Final Thought

The global financial system is evolving.

Banks remain powerful actors, but they are no longer the only players in the game.

Digital infrastructure is expanding the possibilities for how value moves through the economy.

Whether through traditional institutions or emerging networks, the future of finance will likely be defined by systems that offer:

reliability

transparency

scalability

accessibility

So the next time someone says:

“Bark if you love your bank.”

It may be worth asking a different question instead:

What kind of financial system do we want for the next century?

🐕💥 BSV: BARK IF YOU LOVE YOUR BANK — Official Article NFT Cover

A bold satire of the modern financial system.

Banks demand trust… while the system quietly owns your money.

This cover captures the moment the question flips…