Title:Irresponsible Freedom Thrown into the Jungle of the M…

Title:Irresponsible Freedom Thrown into the Jungle of the Market: The SEC’s "Cutting the Arrowhead" Administration

Overview

ㅡRecently, the U.S. Securities and Exchange Commission (SEC) established a monumental, yet profoundly cunning, milestone in the crypto-asset market. On March 17, 2026, the SEC officially classified 16 assets, including Bitcoin (BTC), Ethereum (ETH), XRP, and Bitcoin SV (BSV), as "Digital Commodities." The decisive criterion for this classification was the "Efforts of Others"—a core element of the Howey Test. The logic is that decentralized assets driven by their own protocols, rather than relying on the management capabilities of a specific issuer, have evolved beyond "investment contracts" and are now general commodities rather than "securities" bound by securities law.

The Architect and the Hidden Intent

The architect of this massive shift is the new SEC Chairman, Paul Atkins. Immediately after taking office in January 2026, he firmly declared, "There are no government subsidies or special privileges in the crypto market." His policy is to leave the success or failure of the market solely to technical utility and the cold choice of the market. While this appears to be a revolutionary move to clear regulatory uncertainty, it is, in reality, a declaration of total evasion of responsibility, signaling that the government will no longer intervene in future market chaos or investor losses.

A Turning Point for Bitcoin SV (BSV)

This shift has provided a powerful opportunity for a reversal for BSV, which had been undervalued amidst legal controversies. Although individual past disputes have not completely vanished, the fact that the SEC explicitly listed BSV as a "commodity" has effectively removed the legal and regulatory hurdles preventing major global exchanges from listing it. BSV has now shed its regulatory shackles and entered the arena for a true showdown.

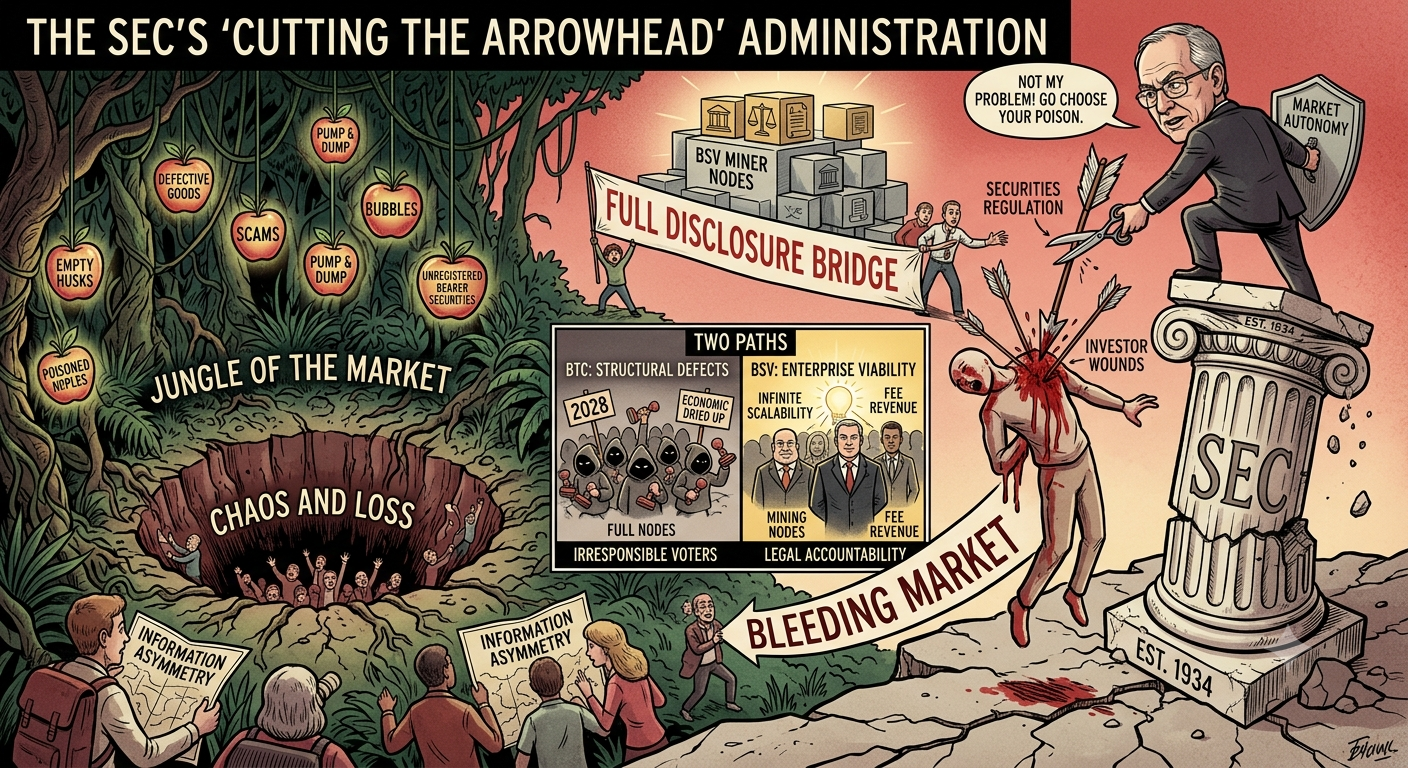

"Cutting the Arrowhead" and the Duty of Protection

The market will now be flooded with products of all stripes: high-quality goods, defective ones, "ugly but tasty" ones, and "empty husks" that look good but lack substance. In this process, the SEC has quietly slipped away from the scene, leaving behind only a chilling warning that "securities"—which it treats as "painted rice cakes" (immaterial illusions)—must not be listed. This is no different from "cutting the arrowhead" (superficial treatment): merely lopping off the visible part of an arrow while ignoring the wound festering deep inside.

However, the SEC has an undeniable "duty of investor protection" as stipulated in the Securities Act of 1933 and the Securities Exchange Act of 1934. Unless they strengthen Full Disclosure to bridge information asymmetry and strictly manage the duty of explanation, the current commodity classification will ultimately result in aiding and abetting massive "misselling" (improper sales practices).

Structural Defects: BTC vs. BSV

The current Bitcoin (BTC) system, in particular, suffers from serious structural flaws. BTC’s so-called "Full Nodes" often act as mere rubber stamps rather than taking actual responsibility for the network. As Dr. Craig Wright (CSW) once warned, this recreates the evils of "unregistered bearer securities" with unclear accountability in the digital world.

In contrast, BSV’s mining nodes differ fundamentally from BTC in terms of "perpetual economic viability" and "accountability":

Node Roles: While BTC is structured with many irresponsible "voters," BSV is centered around "Enterprise Miners" who generate actual blocks and bear legal responsibility.

Validation Consistency: BTC is excessively conservative regarding protocol changes and faces a crisis where economic incentives may dry up after the 2028 halving. Conversely, BSV is proving the self-sustaining viability of its nodes by securing a transaction fee revenue structure through infinite scalability.

* Accountability: Unlike BTC, which hides behind anonymity and claims "it’s no one’s responsibility," BSV emphasizes mutual monitoring among nodes and technical proof within a legal framework.

Conclusion

Ultimately, the gift of "freedom" the SEC has tossed into the market is a cruel homework assignment where consumers must identify the poisoned apples themselves. If the regulator hides behind the shield of "market autonomy" while abandoning its inherent legal duty of consumer protection, the damage will fall entirely on the public—the information-disadvantaged. The ball is now in the market’s court, but the SEC’s eyes—which must monitor whether that market operates justly—must never be closed.